Current Fuse,Auto Fuse,Car Fuse,Blade Fuse Dongguan Andu Electronic Co., Ltd. , https://www.idoconnector.com

After a press conference in Taiwan on February 11th, just one week later, on February 18th, Veeco continued to blow the industry in mainland China close to Taiwan.

Jeffrey, Senior Director, Global Market Communications, Veeco

Jeffrey, senior director of global market communications at Veeco, said at the Shenzhen press conference that they are still very optimistic about the future of MOCVD, and China remains the most promising market. According to Veeco's 2013 fiscal year report, the giant's revenue was $332 million, down 35.7% from last year. Net profit also plummeted from a profit of $30.93 million in 2012 to a loss of $42.26 million.

Benefiting from the rapid increase in demand in the downstream lighting market, the overcapacity problem of LED upstream chips in China has eased in 2013, but there is still a long way to go before the supply and demand reversal.

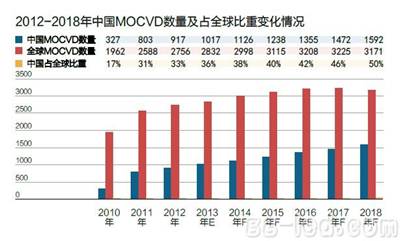

The statistics of the High-tech LED Industry Research Institute (GLII) show that in 2013, China's MOCVD operating rate and capacity utilization rate increased to about 70% and 52% respectively. In 2013, domestic MOCVD reached 1017 units, an increase of 11% year-on-year. Considering that there is still a lot of room for release of existing capacity and the market is becoming more rational, GLII expects that the MOCVD equipment in China's LED market will show a smooth and stable growth trend in the future.

(Data from the High-tech LED Industry Research Institute)

However, with the gradual increase in the market share of the epitaxial chip manufacturers in the first echelon, Taiwan's chip factories are generally under pressure, and capacity expansion to reduce costs is imminent. The scale competition of the two extension factories will also bring certain orders to MOCVD manufacturers to a certain extent.

On January 7, 2014, Sanan Optoelectronics' additional issuance was officially approved by the China Securities Regulatory Commission. Wang Qing, director of Sanan Optoelectronics, said that the funds raised this time will be used to introduce 100 sets of MOCVD machine equipment for the second phase of Wuhu Optoelectronics Industrialization. After the project is completed, it is expected to produce 1.223 million pieces of LED epitaxial wafers (4 inches). , blue and green chips of 25.614 billion tablets. On February 17, 2014, Taiwan's largest chip factory, Jingyuan Optoelectronics, Taiwan's Miaoli Zhunan Science Park N9 new plant started construction, and it is the seat of the world's largest LED chip factory.

The larger market space comes from the rapid release of demand in the terminal lighting market. With the reduction in lighting costs, the popularity of LED general lighting is changing. According to the statistics of the High-tech LED Industry Research Institute (GLII), the scale of China's LED application industry reached 208.1 billion yuan in 2013, a year-on-year increase of 31%. It is estimated that the output value of indoor and outdoor functional lighting of LEDs in China will exceed 100 billion yuan in 2014. The indoor and outdoor functional lighting of LED will continue to expand in 2013.

Now the cost of LED lighting has dropped far faster than the US Department of Energy forecast, and the price has now reached 6-7$/lm. Government and industry support for the LED market will help the growth of MOCVD market demand, and the application of LED in backlight and display has been saturated after years of development, so LED lighting will be the key point to drive the next wave of market demand.

Jeffrey cited third-party data to show that the number of MOCVD machines required for the universalization of LED general illumination is still large. It is estimated that the number of MOCVD devices required for mobile phones will reach 250 in 2020, and the number of MOCVD devices required for LED TV backlight applications will reach 1,500 MOCVD. With the continuous growth of the general lighting field, the number of MOCVD units required for LED lighting will reach thousands, and these are all opportunities for Veeco in the future, even though the current penetration rate of lighting is only 5%.

In fact, the demand for MOCVD orders in the short-term LED lighting demand is still relatively stable. In addition, some solutions to optimize the productivity of existing MOCVD equipment also bring a lot of pressure on equipment demand growth.

According to the HVPE system released by GTAT to replace the nGaN and uGaN growth processes in MOCVD, more than 80% of the consumption of consumables such as chip gas can be saved. After the HVPE system is used in the chip factory, the crystal growth rate will increase significantly, and the MOCVD capacity will be increased. At the same time, the LED chip factory with the HVPE system expansion capacity can save more than 25% of the comprehensive cost. ![]()

[Text / Long Zonghui] For the two international giants that almost monopolize the MOCVD market, the most profitable years in Asia, especially in the Chinese market, have become memories. Since the second half of 2012, the local government subsidies have been shut down, the lighting market demand is lower than expected, and the domestic MOCVD manufacturers have exerted their strength. One after another, the “redemption†has become the top priority of the two MOCVD giants this year, a difficult market. The defense battle has started.